English

English

2023: a year that thwarted (almost) all predictions

2023 was a surprising year, full of twists and turns that no one could have predicted. Against a backdrop of inflation and unprecedented rate hikes in the developed economies, investors initially benefited from a very positive start to the year. Then came the spectre of a banking crisis, first in the United States and then in Europe, before disappearing, taking with it three US regional banks and above all the European giant Crédit Suisse.

The rise of artificial intelligence propelled technology stocks to new heights, while strong pressure on bond yields caused significant volatility on the markets.

Although questioned at the outset, the assumption of a fall in inflation and a soft landing for the economy gained consensus by the end of the year. This optimistic outlook, combined with expected interest rate cuts over the coming year, generated a spectacular rebound in both bonds and equities, enabling us to end 2023 with returns well above expectations.

Looking back on this tumultuous year, Birdee would like to take you through the issues that have influenced the performance of your portfolios and provide you with some key information to start 2024 with as few worries as possible.

Inflation and interest rates, the main causes of volatility

The central banks’ battle against inflation, which began in 2022, dominated much of the economic news in 2023. Whether in the United States, Europe or the United Kingdom, central banks on both sides of the Atlantic successively pushed interest rates to record levels. The aim? To reduce inflationary pressures to below the 2% annual increase threshold. Higher interest rates restrict access to financing for businesses and individuals, gradually cooling the overheating economy and slowing the rise in prices.

While central banks’ tools and objectives were similar in the United States and Europe, the economic dynamics of the two markets were very different. The massive fiscal stimulus implemented by the Biden administration and the considerable increase in government debt, enabling major investment, significantly contributed to the US economy’s resilience. Despite successive hikes, bringing interest rates to 5.5%, growth figures were well above estimates and the labour market remained extremely tight before weakening slightly at the very end of the year. Despite these macroeconomic data pointing to an inflationary environment, price rises slowed a little, eventually halving in comparison to the start of the year.

Europe is certainly the region where analysts’ predictions came closest to economic reality. In the absence of measures similar to those taken in the United States, the European market suffered from anaemic growth, more weighed down by an energy shock that was considerably greater than on the other side of the Atlantic. Despite more pessimistic macroeconomic figures, inflation remained tenacious in the Union. Like its American counterpart, the European Central Bank (ECB) had to raise interest rates successively above 4% in order to effectively curb runaway inflation.

While at the start of the year, investors’ main objective was to estimate the extent of rate hikes, from the second half of the year onwards, discussions focused more on the relatively late arrival of a pause in monetary policy, to then gamble on a timetable for easing financing conditions in 2024. Whatever the nature of the discussions on interest rates, investors’ expectations and their responses to the strategies adopted by the central banks created the climate on the financial markets: expectations of rate rises or macroeconomic figures pointing in that direction sent the markets plummeting (Q3), while more optimistic prospects for a halt to rate rises generated spectacular rebounds (November and December). This pattern, together with often contradictory macroeconomic data, acted as a catalyst for market volatility.

The United States and Japan celebrated, Europe was in slight decline and China struggled

Two geographical regions came out on top in 2023. However, the reasons for these successes are quite different...

The United States, which, as we mentioned earlier, benefited from a very robust economic environment, was the big winner on the financial markets. But these macroeconomic factors were far from being the main driver of performance. In fact, it was the big technology companies, referred to by investors as ‘The Magnificent Seven¹’, that propelled most of the major US indices to new heights. Massive investment by these companies in the high-profile field of artificial intelligence was a major factor in their success. The Nasdaq, which is heavily weighted towards the technology sector, posted an exceptional annual return of 43.4%, while the S&P500, which is more representative of the US economic landscape as a whole, ended the year with a return of 24.2% in 2023.

Japan, another market that performed well, was an exception among the developed economies in that the Japanese Central Bank maintained a very accommodating monetary policy throughout the year. Far less affected by the inflationary trend impacting on other developed economies, the Japanese market, where most companies are strong exporters, took full advantage of a low local currency and corporate reforms aimed at maximising efficiency. The Nikkei 225 index ended the year with a performance of 28.2%.

In Europe too, the performance of the various stock market indices came as a pleasant surprise. Initially buoyant at the start of the year, European stock markets fell sharply in the third quarter, raising fears of negative returns over the year. These fears were put to rest, however, by the spectacular rebound that began at the end of October with renewed optimism that interest rates would soon fall, ending the year on a very positive note. Still, investors shouldn’t let these high returns distract them from an economic situation that is far more fragile than in the US or Japan. This situation will be a major focus of attention in 2024, as we shall see below.

While things looked rosy for stock markets in continental Europe, this was less the case in the UK. Suffering the full force of the inflationary surge while struggling with the economic consequences of Brexit, the London stock market ended the year in sharp contrast with a very modest return.

|

Index |

Returns in 2023 |

|

Euro Stoxx 50 |

19.2% |

|

CAC 40 |

16.5% |

|

Xetra - DAX |

20.3% |

|

FTSE 100 |

3.8% |

The unpleasant stock market surprise of 2023 came from China. The long-awaited revival of the economy after three years of ‘Zero Covid’ policy failed to materialise. Worse still, the economy was rocked by a major property crisis. Weaker-than-expected growth, heightened geopolitical tensions, the growing competitiveness of other Asian stock markets and government measures deemed too timid by investors all contributed to 2023 being a mediocre year for Chinese markets. The CSI 300² index ended the year with a return of -11.38%.

Responsible investment, between politicisation and regional contrasts

After a very complicated year in 2022, in terms of returns, responsible investment had another eventful year... this time on the political front.

The international political scene became increasingly polarised, providing a platform for the most extreme voices on the political landscape. One country in particular has set the tone: the United States. Like so many other issues, the ESG agenda was directly impacted by the struggles between liberals and conservatives. This ideological battle crystallised around the growing importance of sustainability considerations in the investment choices of companies and individuals. This was followed by a series of measures known as ‘anti-ESG’ in states considered to be Republican strongholds. The stated aim of these measures was to penalise economic players who incorporate ESG factors (or exclude economic sectors that are the most harmful to the environment, such as the fossil fuel sector) in their investment decision process, in the name of free enterprise and the protection of the domestic employment market.

This hostility to ESG considerations is a major challenge in the US, where companies and asset managers are adopting a much more moderate (if not neutral) stance when it comes to voting on measures relating to sustainability issues, for fear of damaging their reputation among a significant section of public opinion. There has therefore been resistance among those whose mantra is ‘profit first’...

In Europe, despite the regulatory obstacles put in place by the most conservative parties, the trend remains much more positive towards sustainable finance. The vast majority of capital for sustainable and responsible investments is raised in Europe, which is implementing the most ambitious decarbonisation plans. Unlike the United States, European public authorities are not hesitating to introduce interventionist measures to encourage the development of strategic sectors where, on the other side of the Atlantic, the unfettered market remains a dominant ideology.

The turmoil surrounding responsible investment should prompt the sector to look inward. Criticism will not stop overnight, depending on the political leanings of the moment. It is the sector’s responsibility to demonstrate transparently not just the usefulness but the absolute necessity of a thorough overhaul of our economies. This burden of proof cannot be satisfied with press releases and pious intentions; it will have to be much more concrete, with the presentation of tangible effects both in terms of sustainability objectives and through the materialisation of the competitive advantages of companies active in the key sectors of climate risk mitigation and the energy and social transition.

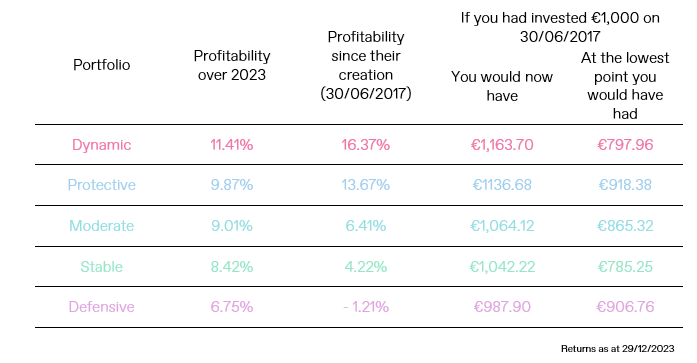

The performance of our portfolios in 2023

Birdee portfolios recorded positive returns in 2023.

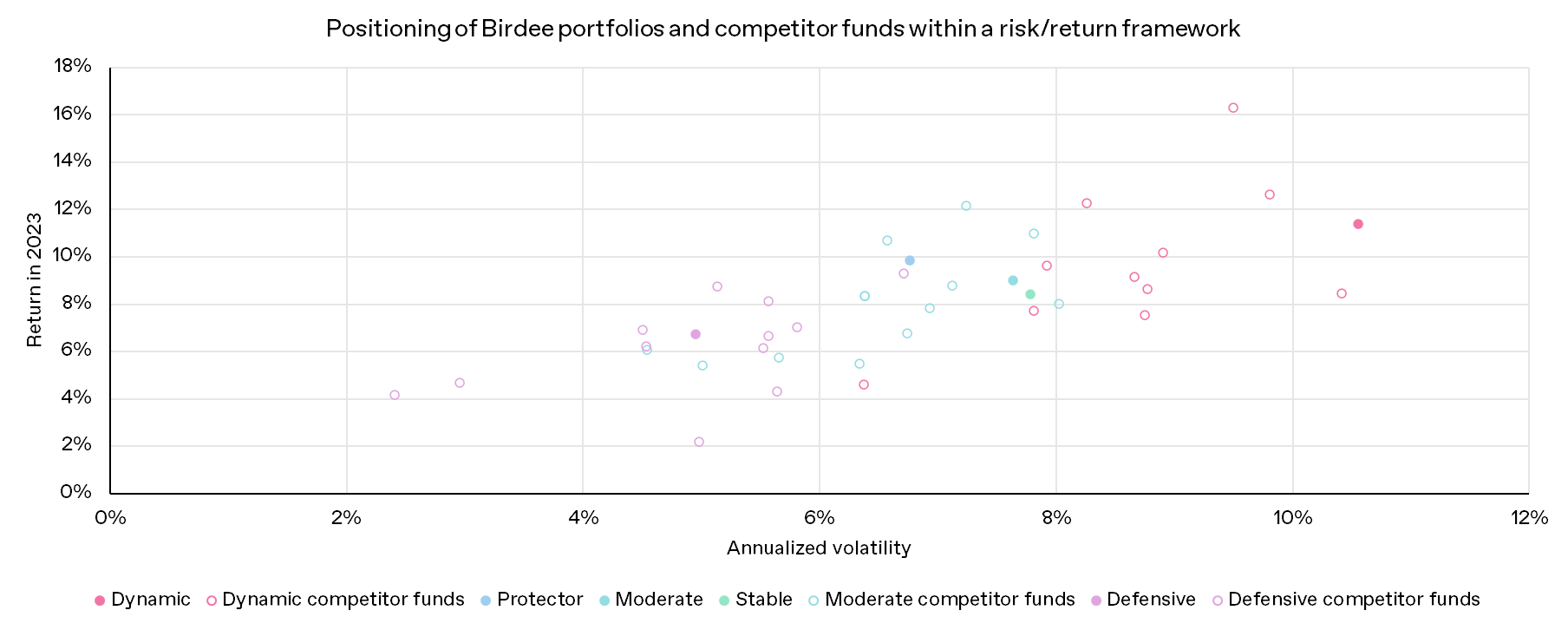

Unsurprisingly, the Dynamic portfolio ended the year with the best returns. Its greater exposure to equities made it more responsive to the various rebounds seen during the year, which had a positive impact on its performance in 2023, particularly in the final weeks of the year when the stock market rally was spectacular after a full quarter of pessimism and sluggish performance. The Dynamic portfolio was also well positioned in relation to competing profiled funds. Although slightly more volatile, the portfolio’s returns were among the highest.

While it’s true that the Dynamic portfolio was the best performer, the other Birdee portfolios were not left behind. It is important to note that the performance of the Moderate portfolio and its Protective and Stable satellites was very close to that of the Dynamic portfolio (with the Protective portfolio holding its own). These three portfolios remained competitive compared with funds of similar risk, with a special mention again for the Protective portfolio, which demonstrated a particularly attractive risk/return profile in 2023.

Lastly, slightly behind but still close to its counterparts with greater exposure to market risk, the Defensive portfolio ended 2023 with a respectable performance. And this portfolio didn’t lag behind its competitors either. It managed to generate competitive returns while maintaining a level of risk below that of most of its competitors.

What explains the low dispersion of performance between the different profiles? Following on from 2022, the atypical economic environment investors faced was characterised by a positive correlation between equities and bonds, asset classes which generally move in opposite directions. In 2022, this phenomenon heavily penalised diversified portfolios. In 2023, the opposite was true. The euphoria of a possible interest rate cut in 2024 and the prospect of a victory over inflation without major damage to the economy were (very) positive signals for equities and bonds.

Another 2022 trend that continued into 2023 (to a lesser extent, thanks to the strong technological component of these funds) was the difficulty for responsible assets to achieve performance levels equivalent to traditional indices. Although this trend was less marked than in 2022, it was still present, and an attempt to explain it can be based on two very distinct factors. Firstly, financing costs for businesses continued to rise before stabilising in the fourth quarter. It goes without saying that these restrictive conditions do not favour growth companies that focus on the major ecological and social issues of our time. Secondly, the geopolitical context was still very tense, with an increase in the number of conflicts and a sharp rise in economic protectionism, meaning high volatility and a tendency for investors to redirect their capital towards so-called ‘safe investments’, often giving little thought to sustainability and responsibility...

Same pattern in 2024?

Will 2024 be similar to 2023 or should we prepare for a major change in market trends? While it’s impossible to predict the future, we’d like to take a look at some of the key factors that are likely to play a major role in the coming year.

Pragmatism is called for in 2024. Investors are well aware that the very good performance of the various stock markets at the end of 2023 is mainly due to the consensus that interest rates will fall very soon. Macroeconomic data, especially in Europe, paints a less happy picture. The fight against inflation seems to be producing results, but at the cost of weak growth and even a slight recession in some economies. In the United States, growth remains positive but has fallen slightly in recent weeks. A resurgence in inflation or worsening macroeconomic figures could therefore shake investor confidence in a soft landing for the economy. Caution is therefore called for in relation to equities. Conversely, a fall in interest rates could benefit bonds, as their price moves in the opposite direction to interest rates.

2024 will also be a political year. Numerous elections will be held over the next twelve months, including the presidential elections in the United States and the parliamentary elections in the European Union. The polls will also be open in India, Taiwan, South Africa and Pakistan, among others. It is highly likely that we will see peaks of tension in the run-up to these elections, which will punctuate the coming year, but also reactions on a scale that will depend on the results more or less anticipated by economic players. While these political events will have a short-term impact on the financial markets, the medium- and long-term effects should not be overlooked. In an extremely tense geopolitical context, the stakes of these elections are all the higher. Friction and supply difficulties linked to increasingly protectionist trends, the radicalisation of certain types of political discourse and its consequences for the economic policies of the countries concerned, as well as the importance of the energy transition and mitigation of climate risks will all be crucial issues in these elections.

As a case in point, let’s talk about sustainability. In 2024, as previously stated, responsible investment will have to mature if it is to revive flagging levels of funding. Europe, which is at the forefront in this field, will continue to legislate to ensure ever greater transparency in capital allocation and enhanced investor protection. The concept of dual materiality will certainly be given greater prominence. In the context of responsible investment, dual materiality expresses the fact that an economic player must not only communicate the impact of ecological and social externalities on its activity, but must also calculate and make public its own impact on these same externalities. Increasing attention is also being paid to the risks associated with social inequalities, and it would be logical to observe a willingness on the part of the various legislators to make this a material consideration in their communications to the various stakeholders.

Protecting the environment, the energy transition and health will undoubtedly feature prominently in discussions about responsible investment. The technology sector will also have an important role to play in developing solutions to the various environmental and social challenges. What’s more, the beneficial effects of the Inflation Reduction Act in the United States and the European Green Deal, which aim to redirect large amounts of funding towards sustainable activities (particularly the energy transition), should continue to be felt over the coming years.

Lastly, a less restrictive monetary policy should benefit responsible investment, which is mainly made up of assets known as ‘growth’ assets whose value is calculated on the basis of estimated future returns discounted at the current interest rate (the lower the rate, the higher the present value).

As we can see, the year ahead holds its share of challenges, but also opportunities. The prospect of a volatile environment, with equities and bonds once again showing a negative correlation, makes it more important than ever to diversify investment portfolios. An investment horizon that is consistent with your objectives is also essential to guard against net losses in turbulent times.

We wish you all the best for 2024! Health, happiness and success!

We would also like to thank you for your confidence in Birdee and, as always, we will be happy to answer any questions you may have.

The Birdee team.

1. Namely: Amazon, Alphabet (Google), Apple, Meta, Microsoft, Nvidia and Tesla..

2. The CSI 300 index comprises the 300 largest companies listed on the Shanghai and Shenzhen stock exchanges.